2025 Prepreg Composite Manufacturing Industry Report: Market Dynamics, Growth Projections, and Strategic Insights. Explore Key Trends, Regional Opportunities, and Competitive Analysis for the Next 5 Years.

- Executive Summary & Market Overview

- Key Technology Trends in Prepreg Composite Manufacturing

- Competitive Landscape and Leading Players

- Market Growth Forecasts (2025–2030): CAGR, Revenue, and Volume Analysis

- Regional Market Analysis: North America, Europe, Asia-Pacific, and Rest of World

- Future Outlook: Emerging Applications and Investment Hotspots

- Challenges, Risks, and Strategic Opportunities

- Sources & References

Executive Summary & Market Overview

Prepreg composite manufacturing refers to the production of fiber reinforcements pre-impregnated with a resin system, typically used in high-performance applications across aerospace, automotive, wind energy, and sporting goods industries. The global prepreg market is poised for robust growth in 2025, driven by increasing demand for lightweight, high-strength materials and advancements in manufacturing technologies. According to MarketsandMarkets, the global prepreg market size was valued at approximately USD 8.1 billion in 2023 and is projected to reach USD 10.5 billion by 2025, registering a CAGR of around 13% during the forecast period.

The aerospace and defense sector remains the largest consumer of prepreg composites, accounting for over 50% of total demand, as manufacturers seek to reduce aircraft weight and improve fuel efficiency. The automotive industry is also emerging as a significant growth driver, with electric vehicle (EV) manufacturers increasingly adopting prepreg composites for structural and body components to enhance performance and range. Additionally, the wind energy sector is witnessing heightened adoption of prepreg materials for turbine blades, supported by global renewable energy targets and investments.

Regionally, North America and Europe dominate the prepreg composite manufacturing market, owing to the presence of major aerospace OEMs and a mature composites supply chain. However, Asia-Pacific is expected to witness the fastest growth through 2025, fueled by expanding aerospace, automotive, and wind energy industries in China, India, and Southeast Asia. Key players such as Hexcel Corporation, Toray Industries, Inc., and SGL Carbon are investing in capacity expansions and R&D to cater to evolving industry requirements and regulatory standards.

- Technological advancements, such as automated fiber placement (AFP) and out-of-autoclave (OOA) curing, are enhancing production efficiency and reducing costs.

- Stringent environmental regulations are prompting the development of bio-based and recyclable prepreg systems.

- Supply chain disruptions and raw material price volatility remain key challenges for manufacturers in 2025.

In summary, the prepreg composite manufacturing market in 2025 is characterized by strong demand from high-growth sectors, ongoing technological innovation, and a shifting regional landscape, positioning it as a critical enabler of next-generation lightweight engineering solutions.

Key Technology Trends in Prepreg Composite Manufacturing

Prepreg composite manufacturing is experiencing rapid technological evolution as industries such as aerospace, automotive, wind energy, and sports equipment demand higher performance, lighter weight, and greater production efficiency. In 2025, several key technology trends are shaping the landscape of prepreg composite manufacturing, driving both innovation and competitiveness.

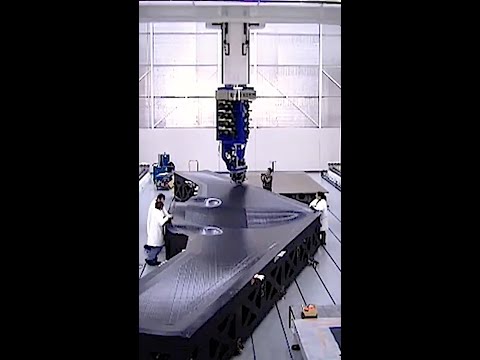

- Automation and Digitalization: The integration of automation, robotics, and digital process control is transforming prepreg manufacturing lines. Automated tape laying (ATL) and automated fiber placement (AFP) systems are increasingly adopted to improve precision, reduce labor costs, and enable high-volume production. Digital twins and real-time process monitoring are being used to optimize curing cycles and quality assurance, as reported by CompositesWorld.

- Out-of-Autoclave (OoA) Processing: Traditional autoclave curing is energy-intensive and costly. In 2025, OoA technologies—such as vacuum bag only (VBO) prepregs—are gaining traction, especially for large structures in aerospace and wind energy. These methods reduce capital investment and enable the production of larger, more complex parts, according to SGL Carbon.

- Advanced Resin Systems: The development of new resin chemistries, including toughened epoxies, thermoplastics, and bio-based resins, is enhancing the mechanical properties, durability, and sustainability of prepregs. Fast-curing and low-temperature curing resins are enabling shorter cycle times and expanding the range of applications, as highlighted by Hexcel Corporation.

- Customization and On-Demand Manufacturing: Digital manufacturing platforms and modular prepreg lines are allowing for greater customization of fiber orientation, resin content, and part geometry. This trend supports the growing demand for tailored solutions in niche markets, as noted by Toray Industries.

- Sustainability Initiatives: Environmental concerns are driving the adoption of recyclable thermoplastic prepregs, bio-based resins, and closed-loop manufacturing processes. Companies are investing in greener supply chains and end-of-life recycling solutions, in line with sustainability goals outlined by Teijin Limited.

These technology trends are expected to accelerate the adoption of prepreg composites across industries, reduce production costs, and support the development of next-generation lightweight structures in 2025 and beyond.

Competitive Landscape and Leading Players

The competitive landscape of the prepreg composite manufacturing market in 2025 is characterized by a mix of established multinational corporations and innovative regional players, all vying for market share in a sector driven by demand from aerospace, automotive, wind energy, and sporting goods industries. The market is moderately consolidated, with a handful of key players accounting for a significant portion of global production capacity and technological advancements.

Leading the market are companies such as Hexcel Corporation, Toray Industries, Inc., and SGL Carbon. These firms have established robust supply chains, extensive R&D capabilities, and a global footprint, enabling them to serve major OEMs and tier-1 suppliers across multiple end-use sectors. Hexcel Corporation and Toray Industries, Inc. in particular have made significant investments in expanding their prepreg production facilities in North America and Europe to meet the growing demand from the aerospace and defense sectors, which remain the largest consumers of high-performance prepregs.

Other notable players include Solvay S.A., Teijin Limited, and Park Aerospace Corp., each leveraging proprietary resin systems and fiber technologies to differentiate their product offerings. Solvay S.A. has focused on developing advanced thermoplastic prepregs, targeting the automotive and industrial sectors for lightweighting applications. Meanwhile, Teijin Limited has expanded its global reach through strategic acquisitions and partnerships, particularly in Asia-Pacific, which is emerging as a high-growth region for prepreg consumption.

- Hexcel Corporation: Focuses on aerospace-grade carbon fiber prepregs and has expanded capacity in the U.S. and Europe.

- Toray Industries, Inc.: Offers a broad portfolio of carbon and glass fiber prepregs, with a strong presence in both aerospace and industrial markets.

- SGL Carbon: Specializes in carbon fiber-based prepregs for automotive and wind energy applications.

- Solvay S.A.: Innovates in thermoplastic and thermoset prepregs, with a focus on sustainability and recyclability.

- Teijin Limited: Expanding in Asia-Pacific, with a focus on high-performance and specialty prepregs.

Competition is intensifying as companies invest in automation, digitalization, and sustainable manufacturing practices to reduce costs and environmental impact. Strategic collaborations, mergers, and acquisitions are expected to continue shaping the market dynamics through 2025, as players seek to enhance their technological capabilities and global reach.

Market Growth Forecasts (2025–2030): CAGR, Revenue, and Volume Analysis

The prepreg composite manufacturing market is poised for robust growth in 2025, driven by increasing demand from aerospace, automotive, wind energy, and sporting goods sectors. According to projections by MarketsandMarkets, the global prepreg market is expected to register a compound annual growth rate (CAGR) of approximately 10% from 2025 through 2030. This growth trajectory is underpinned by the rising adoption of lightweight, high-strength materials to improve fuel efficiency and reduce emissions, particularly in aerospace and automotive applications.

Revenue forecasts for 2025 indicate that the global prepreg composite manufacturing market will surpass USD 8.5 billion, with North America and Europe maintaining their dominance due to established aerospace and automotive industries. The Asia-Pacific region, however, is anticipated to exhibit the fastest growth, propelled by expanding wind energy installations and increasing investments in electric vehicles and infrastructure projects. By 2030, the market is projected to reach over USD 13.5 billion, reflecting sustained demand and technological advancements in resin systems and fiber reinforcements.

In terms of volume, the market is expected to exceed 120 kilotons in 2025, with carbon fiber prepregs accounting for the largest share due to their superior mechanical properties and widespread use in high-performance applications. Glass fiber prepregs will also see steady growth, particularly in wind turbine blades and marine applications, where cost-effectiveness and corrosion resistance are critical. The volume demand is forecasted to grow at a CAGR of 8–9% through 2030, with significant contributions from emerging markets in Asia and Latin America.

- Aerospace: The sector will continue to be the largest consumer, with OEMs and tier suppliers increasing their reliance on prepregs for primary and secondary structures (Global Industry Analysts, Inc.).

- Automotive: Adoption will accelerate, especially in electric vehicles, as manufacturers seek to offset battery weight and meet stringent emission standards.

- Wind Energy: The push for renewable energy will drive demand for glass and carbon fiber prepregs in turbine blade manufacturing.

Overall, the prepreg composite manufacturing market in 2025 is set for dynamic expansion, with innovation in materials and processing technologies further enhancing market penetration and revenue growth across key end-use industries.

Regional Market Analysis: North America, Europe, Asia-Pacific, and Rest of World

The global prepreg composite manufacturing market is characterized by distinct regional dynamics, with North America, Europe, Asia-Pacific, and the Rest of the World (RoW) each exhibiting unique growth drivers, end-use trends, and competitive landscapes for 2025.

North America remains a dominant force, driven by robust demand from the aerospace, defense, and automotive sectors. The presence of major aircraft manufacturers and a strong focus on lightweight, fuel-efficient vehicles underpin market expansion. The U.S. government’s continued investment in defense modernization and the adoption of advanced materials in commercial aviation further stimulate growth. According to MarketsandMarkets, North America is expected to maintain a significant market share, with the U.S. leading in both consumption and technological innovation.

Europe is characterized by stringent environmental regulations and a strong emphasis on sustainability, which drive the adoption of prepreg composites in automotive and wind energy applications. The region’s well-established aerospace industry, particularly in France, Germany, and the UK, continues to be a major consumer. The European Union’s Green Deal and initiatives to reduce carbon emissions are accelerating the shift toward lightweight materials. According to Grand View Research, Europe is projected to witness steady growth, with increasing investments in renewable energy infrastructure and electric vehicles.

Asia-Pacific is anticipated to be the fastest-growing region, fueled by rapid industrialization, expanding aerospace manufacturing, and a burgeoning automotive sector. China, Japan, and South Korea are at the forefront, with significant investments in high-speed rail, wind energy, and next-generation aircraft. The region’s cost-competitive manufacturing base and government incentives for advanced materials adoption are key growth enablers. Fortune Business Insights highlights that Asia-Pacific’s prepreg market is set to outpace other regions in terms of CAGR through 2025.

- Rest of the World (RoW) includes Latin America, the Middle East, and Africa, where market penetration is comparatively lower but rising. Growth is primarily driven by increasing investments in infrastructure, wind energy, and emerging aerospace projects, particularly in Brazil and the UAE. However, limited local manufacturing capabilities and higher import dependence may restrain rapid expansion.

Overall, regional market dynamics in 2025 reflect a blend of mature demand in North America and Europe, rapid expansion in Asia-Pacific, and emerging opportunities in RoW, collectively shaping the global prepreg composite manufacturing landscape.

Future Outlook: Emerging Applications and Investment Hotspots

The future outlook for prepreg composite manufacturing in 2025 is shaped by a convergence of technological innovation, expanding end-use applications, and shifting investment priorities. As industries increasingly prioritize lightweight, high-strength materials for performance and sustainability, prepreg composites are poised for robust growth across several sectors.

Emerging Applications

- Electric Vehicles (EVs): The automotive sector, particularly EV manufacturers, is accelerating the adoption of prepreg composites to reduce vehicle weight and extend battery range. Advanced thermoset and thermoplastic prepregs are being integrated into structural and semi-structural components, with companies like Tesla and BMW Group investing in composite-intensive platforms.

- Urban Air Mobility (UAM): The rise of eVTOL (electric vertical takeoff and landing) aircraft is creating new demand for lightweight, high-performance prepregs. Startups and established aerospace players are leveraging these materials to meet stringent safety and efficiency requirements, as highlighted by Airbus and Joby Aviation.

- Wind Energy: The wind power sector is scaling up blade sizes, necessitating advanced prepreg solutions for longer, more durable blades. Vestas and Siemens Gamesa are investing in next-generation prepreg technologies to enhance blade performance and lifecycle.

- Sports and Consumer Goods: High-end sports equipment and premium consumer products continue to adopt prepreg composites for their superior strength-to-weight ratio and design flexibility, with brands like Trek Bicycle Corporation and Callaway Golf leading the way.

Investment Hotspots

- Asia-Pacific: The region is emerging as a key investment destination, driven by rapid industrialization, government incentives, and the expansion of aerospace and automotive manufacturing hubs in China, Japan, and South Korea (MarketsandMarkets).

- Automation and Digitalization: Investment is flowing into automated prepreg manufacturing lines and digital process controls to boost throughput, consistency, and cost-efficiency. Companies such as Hexcel Corporation and Toray Industries are at the forefront of this trend.

- Recyclable and Bio-based Prepregs: Sustainability concerns are driving R&D and capital allocation toward recyclable resin systems and bio-based fibers, with support from both private investors and public funding initiatives (CompositesWorld).

In summary, 2025 will see prepreg composite manufacturing propelled by new applications in mobility, energy, and consumer markets, with investment clustering around automation, sustainability, and the dynamic Asia-Pacific region.

Challenges, Risks, and Strategic Opportunities

The prepreg composite manufacturing sector faces a complex landscape of challenges and risks in 2025, but these also give rise to significant strategic opportunities. One of the primary challenges is the volatility in raw material prices, particularly for carbon fibers and advanced resins. Fluctuations in the cost of petroleum-based feedstocks and supply chain disruptions—exacerbated by geopolitical tensions and lingering post-pandemic effects—have led to increased production costs and unpredictable lead times. This volatility pressures manufacturers to secure long-term supply agreements and diversify sourcing strategies to mitigate risk (MarketsandMarkets).

Another critical risk is the stringent regulatory environment, especially in aerospace and automotive applications, where prepreg composites are most widely used. Compliance with evolving fire, smoke, and toxicity (FST) standards, as well as environmental regulations regarding volatile organic compound (VOC) emissions, requires ongoing investment in R&D and process innovation. Failure to meet these standards can result in costly certification delays or market exclusion (Grand View Research).

Technological complexity also presents a barrier. The need for precise temperature and humidity control during prepreg production, as well as the requirement for specialized storage and handling, increases operational costs and limits the scalability of manufacturing. Smaller players may struggle to invest in the necessary infrastructure, leading to market consolidation and the dominance of established firms with advanced capabilities (Fortune Business Insights).

Despite these challenges, strategic opportunities abound. The push for lightweighting in transportation—driven by fuel efficiency and emissions reduction targets—continues to expand demand for prepreg composites in automotive, aerospace, and wind energy sectors. Manufacturers that can innovate with bio-based resins or recyclable prepreg systems stand to gain a competitive edge, aligning with sustainability trends and regulatory incentives. Additionally, digitalization and automation in prepreg manufacturing, such as the adoption of Industry 4.0 technologies, offer pathways to reduce costs, improve quality, and enhance supply chain resilience (Research and Markets).

In summary, while prepreg composite manufacturing in 2025 is challenged by supply chain risks, regulatory pressures, and technological demands, companies that proactively address these issues and invest in innovation are well-positioned to capitalize on the sector’s robust growth potential.

Sources & References

- MarketsandMarkets

- SGL Carbon

- CompositesWorld

- Teijin Limited

- Teijin Limited

- Grand View Research

- Fortune Business Insights

- Airbus

- Joby Aviation

- Vestas

- Siemens Gamesa

- Callaway Golf

- Research and Markets